My clients have plenty of questions about Medicaid and long-term care. One of the most common is: Can’t I give $19,000 a year? The answer is clear: not as far as Medicaid is concerned.

This idea comes from tax law. We have a federal gift tax, but you can give up to $19,000 per person in 2025 free of both tax and paperwork. (If you exceed that amount, you have to file a gift tax return so the IRS can reduce your lifetime gift-and-estate-tax exemption. It’s annoying paperwork, but only multimillionaires end up actually owing any tax.) The amount used to be $15,000, so sometimes my clients reference that number.

Regardless, this exemption is a tax rule, not a Medicaid rule. Although both have a lot to do with money and the federal government, tax law and Medicaid law have almost nothing to do with each other. So although you may give $19,000 tax-free, that doesn’t mean the gift is free of Medicaid consequences, too.

In fact, Medicaid law considers almost any gift a divestment and imposes severe consequences. If you gave each of your children $19,000 and needed expensive long-term care within the next five years, Medicaid would deny your application and force you to pay the expensive private rate out-of-pocket for months or even years before you could apply again. The Medicaid office wouldn’t care that tax law made the gift tax-free.

Unfortunately, this myth is so pervasive that many people make large gifts to their families without thinking twice. It’s a natural mistake. The good news is that there are ways to either cure a divestment or deal with its consequences, if you plan ahead and work with an elder law attorney.

I often plan for divestment and its consequences with my clients. Sometimes they’ve unwittingly divested in the past. Sometimes they want to give something to their families and simply need a strategy for the consequences. Sometimes, even, the Medicaid rules allow an asset to be divested, and we want to take advantage of that.

The divestment rules are complicated. They can either save you money or cost you money on the order of tens or hundreds of thousands of dollars. That’s why it makes sense to get help from an expert who understands the rules and knows how to navigate them.

https://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.png00Benjaminhttps://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.pngBenjamin2025-05-13 03:22:012025-05-13 03:22:01Myth: Can’t I give $19,000 a year?

With Medicaid, one small detail can cost you thousands. Take, for example, the recent case of a woman whose husband was on Medicaid for long-term care. She thought she had to spend the money in her bank account, so that’s what she did. Only the problem wasn’t her bank account at all.

You can read all about it at Elder Law in Wisconsin, where I publish Medicaid decisions for other elder law attorneys. The problem was one of those Medicaid details few people understand, even those who work with long-term care and Medicaid daily: the rules about a married couple’s assets are different when you first apply and when you first renew.

When a married couple first applies for long-term care Medicaid, it doesn’t matter whose name is on the assets. With only a few exceptions, the Medicaid office adds up the assets in either spouse’s name. If the total is over the asset limit—which can be anywhere from $52,000 to about $160,000—the application is denied. The Medicaid Eligibility Handbook (the rule book for the county Medicaid office) says: “Count the combined assets of the institutionalized person and his or her community spouse. Add together all countable, available assets the couple owns.”

After the application is approved, however, the rule changes. Now it does matter whose name is on the assets. The couple has one year to get the institutionalized spouse’s name off everything above $2,000. This is called the “asset transfer period.” At the first renewal (Medicaid benefits have a “renewal” every year where you have to update your information and prove you are still eligible), the only thing that matters is that the name of the spouse on Medicaid is on less than $2,000 worth of assets. In fact, the other spouse (the “community spouse”) could have a million dollars and it wouldn’t affect the Medicaid benefits, as long as that million was in his or her sole name. The Medicaid Eligibility Handbook says: “The institutionalized spouse must transfer the assets to the community spouse by the next regularly scheduled review (12 months). If their assets are above $2,000 on the date of the next scheduled review, they will be determined ineligible.” (That’s the singular they, by the way.)

So what happened to the woman in this case? Her husband had his first yearly Medicaid renewal, where it was discovered he still had his name on some stocks. She was told they had too much money to be eligible. Her mistake was thinking that she had to spend down her own bank account rather than the stocks. It’s an understandable mistake, because that would have worked when they first applied. But at the first renewal the rules are different.

In fact, she didn’t have to spend down anything. The problem could have been solved by simply transferring ownership of the stocks from her husband’s name to hers. One phone call with an experienced elder law attorney would have told her that. We don’t know how much money was in her bank account that she spent down. The stocks were worth more than $16,000. Her husband lost Medicaid for two months because of the mistake, so she also had to pay for his long-term care during that time. So, this small detail, this simple, understandable mistake likely cost her several tens of thousands of dollars.

That’s the difference one small detail can make. That’s the difference good advice from an elder law attorney can make. And that’s why one of my core values is be correct. With Medicaid, being correct requires attention to the details.

https://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.png00Benjaminhttps://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.pngBenjamin2025-05-06 16:10:082025-05-06 16:10:08She could have kept her money

There’s a common misconception about asset protection: Protecting my assets saves me money right away. In fact, it protects the assets immediately but only saves you money in the long run.

Here’s what I mean. Remember that asset protection usually means transferring your property to an irrevocable trust and giving up your right to use it. This ensures the property won’t be spent on your own long-term care or recovered by the State after you die—your family will get to keep it. But you don’t transfer everything you own. Whatever isn’t transferred must still be spent on long-term care.

Imagine a single elderly woman who needs nursing home care and has $200,000 in a bank account. If nothing changes, that bank account will be going down by (let’s say) $10,000 per month until it’s all gone (a high estimate, but it makes the numbers easier to comprehend). Medicaid only pays for the care after all $200,000 is spent, which takes 20 months.

What if, in the same situation, $100,000 is in an asset protection trust? That means Medicaid pays for the care after only $100,000 is spent, which takes 10 months. That looks like a good $100,000 saved.

But whether that $100,000 is actually saved or not depends on how long she lives and continues to need care. If she passes away the day after creating the trust, no money has actually been saved; the family gets $200,000, whether half of it is in an asset protection trust or not. If she passes away after 10 months and spending $100,000 on long-term care, again no money has actually been saved; the family gets the remaining $100,000 whether it’s in a trust or not. It’s after this point that money starts being saved (the green zone in the chart below).

caption for image

You can see this in the scenario where she passes away after 15 months:

Scenario 1: She did no asset protection. She will have spent $150,000, leaving $50,000 for the family.

Scenario 2: She protected $100,000 in an asset protection trust. She will have spent $100,000 and then qualified for Medicaid, leaving $100,000 in the asset protection trust for the family.

The difference between Scenario 1 and Scenario 2 is $50,000. That is the money actually saved by asset protection.

Note that the full $100,000 isn’t actually saved until she lives and needs long-term care for a full 20 months. This why it’s best to think of asset protection as a cap on liability, rather than an instant savings coupon.

It’s a bit like health insurance with a deductible. Before asset protection, this woman had a “deductible” of $200,000 before her de facto long-term care insurance (Medicaid) kicked in; after asset protection, this woman had a “deductible” of $100,000. In either case, that deductible must be spent first, and there’s a decent chance she will never need to spend that much.

before asset protection

after asset protection

Why am I explaining this so carefully? It’s important to making an informed decision. Is it worth the work and legal fees to protect assets? Sometimes asset protection is marketed as if it’s a no-brainer: Pay me $5,000 and you’ll save $100,000. The reality is not so simple.

If you’re wondering about asset protection, talk to an elder law attorney to understand how much you can protect. Then think of the amount that isn’t protected. What are the chances you’ll have to burn through it all paying a nursing home? How long would that take?

If you doubt that will ever happen, asset protection might not accomplish much. But if you’re worried about losing all that money and then some, asset protection may be right for you. It will give you the assurance that this much, and no more, will be lost. It will put a cap on the cost of long-term care.

https://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.png00Benjaminhttps://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.pngBenjamin2020-02-05 20:49:012022-01-07 18:41:28How to think about asset protection

“If your business is helping people apply for Medicaid, how do you get paid?”

I’ve heard these and similar comments a number of times. They are often the first questions after I explain what I do. Most people know that Medicaid is a social safety net program providing health insurance to people with very low incomes. If my clients are already poor, how does this work as a business?

Although providing health insurance to those with low income is a big and important part of Medicaid, it is not the only part. Medicaid also pays for the long-term care of elderly people—even those who have middle-class income and assets, if the cost of care exceeds their income. In fact, Medicaid pays for 50 to 60% of all long-term care costs in the United States; it’s the de facto long-term care insurance plan for the middle class. That’s the part of Medicaid I deal with.

Think of it this way: when facing a health care bill of $9,000 per month, we’re all poor.

Medicaid provides a critical safety net not only for low-income people, but also for formerly middle-income people who have spent their life savings paying for long-term services and supports.

So most of my clients are, in fact, middle-class. They come to me once they know they will need long-term care. They look at the cost of a nursing home, look at their life’s savings, and face a simple fact: they may not be poor yet, but they will be. Someone tells them they should look at Medicaid. That’s when they know they need help.

My clients still have money, but are seeing it evaporate rapidly. Without any legal help, they will lose nearly all their savings—they’ll end up with $2,000 if single, or somewhere between $50,000 and $128,000 if they have a spouse. The rest of their money is going away—to pay for one more nursing home bill before Medicaid kicks in, if nowhere else.

My job as a lawyer is to help my clients be proactive. With planning, I can often ensure a good amount of that evaporating money is saved for the spouse, is saved for the family, or is used to provide for my clients’ future needs.

My job is also to take the worrisome task of the Medicaid application, do it well, and do everything in my power to make sure the process goes smoothly. Sometimes I catch and solve problems that would have left a client both penniless and ineligible for Medicaid. When one mistake on a Medicaid application could cost tens of thousands of dollars, it’s worth hiring an attorney to make sure it’s done right.

Even so, often the most valuable thing I do is give my clients peace of mind and clarity. With Medicaid, it’s hard to know just what you can and can’t do, what will and won’t happen, and what resources you can and can’t keep. I answer those questions.

Medicaid is not just for poor people. It is, increasingly, for the elderly middle class who have no other options.

https://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.png00Benjaminhttps://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.pngBenjamin2020-02-05 16:59:402022-01-07 18:42:43Who is Medicaid for?

When it comes to nursing homes and Medicaid, you often hear about “asset protection.” It’s a hot topic—who wouldn’t want to protect their assets? But asset protection is complex, and if something goes wrong your finances and your family could be in a lot of trouble.

Protecting an asset means giving up control.

At its core, asset protection means one thing: transferring legal control of your property to another person. It’s called protection because once you give up your legal right to an asset, you can’t be forced to pay it to your creditors—including hospitals, nursing homes, and the state itself. In other words, the asset is protected. Since so many people—about one third of the elderly—end up paying their entire savings to medical creditors for long-term care, finding a way to protect those savings is attractive. Even though it means giving up your own right to use them.

Note: There’s an important exception to protecting your assets by giving them away. You can’t do it to avoid a debt your currently owe. That’s fraud. Asset protection is all about planning ahead.

Asset protection usually involves an irrevocable trust.

So the idea of asset protection is to transfer legal ownership of your property now before you end up having to pay for long-term care later. The simplest way of doing this is to just give your assets to someone else. You might give your property to a trusted family member, who informally agrees to hold onto the money and give it back to you if you need it. In doing this, though, you give up all legal right to the property. The person you give it to could spend it all on a luxurious vacation. They could also be forced to pay it towards their own debts.

For these reasons, an outright gift is risky. But there’s another way to protect your assets while retaining some control: using an irrevocable asset protection trust. An elder law attorney can create a trust to hold your property under your own terms. You get to make the rules for who gets the property, when, and how.

The cornerstone of an asset protection trust is that you and your spouse cannot retain the right to use the property yourselves. But you can retain the right to say who else gets to use the property, and when. These other people (usually your family) are your beneficiaries.

Usually these trusts are designed to prevent the trust property from being used at all until you and your spouse die. The property isn’t just protected, it’s preserved. This is important because you might still need to dissolve the trust and take back the property.

Even an irrevocable trust can be undone.

But isn’t this trust irrevocable? Yes, but there’s still a legal procedure for dissolving it and distributing its assets—you just can’t do it alone. Doing this requires the consent of all beneficiaries of the trust. Those beneficiaries are probably your children or other family members. It’s a cumbersome procedure that should be done with an attorney and only in an emergency, but it can be done.

Why would you need to dissolve the trust and undo your asset protection? Perhaps an emergency depletes your other savings sooner than expected. Or you need to apply for Medicaid within five years of creating the trust.

Asset protection means divestment.

When you put property into an asset protection trust, you are divesting it. That means if you apply for Medicaid within five years, you’ll have to pay a penalty. But you can “cure” the divestment if the property is given back to you. Again, this requires the cooperation of your beneficiaries.

Asset protection always means giving up your legal right to use assets for your own benefit. That means asset protection always creates a divestment for Medicaid. If not done carefully, you could end up unable to pay for the care you need and ineligible for Medicaid. You do not want to be in that situation.

That’s why you need an elder law attorney to create an effective plan for asset protection. Only an attorney can look at your entire situation and ensure you are provided for, no matter what happens.

https://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.png00Benjaminhttps://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.pngBenjamin2019-11-08 19:57:302022-01-07 18:44:14What is asset protection?

“Do I need a trust?” It’s about the most common question I get. Trusts are one of the most complicated, confusing, and misunderstood pieces of estate planning. In this and following articles, I’m going to break them down and make trusts simple. First up: taking a step back to talk about what a trust is.

A simple trust

Most people think a trust is essentially a bank account. It holds property; you can put property in and take it out. That’s true in some ways, but a trust is much more than a box that holds property. Legally speaking, a trust is a set of relationships between property and people.

To illustrate, imagine:

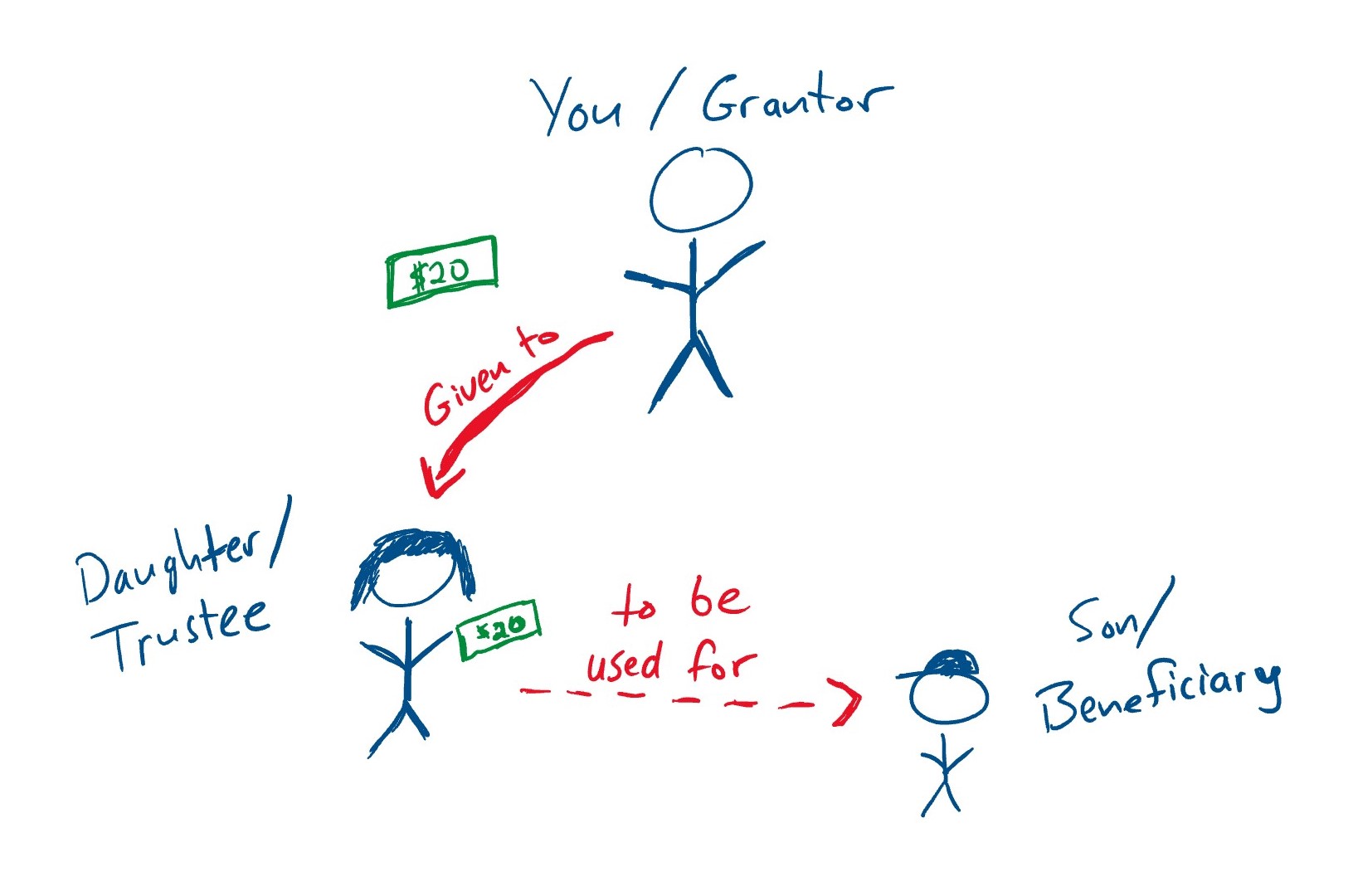

You’ve taken your family to the county fair.

Your 8-year-old son is about to go play some games, supervised by your teenage daughter.

You’ve budgeted $20 for each child to spend during the outing.

You probably wouldn’t hand your 8-year-old $20 and trust he’ll spend it well. You’d probably hand it to your daughter with instructions to make sure it isn’t spent all in one place or too quickly, and to make sure there’s enough left over to buy lunch. You would say you’ve trusted your daughter with that money. You might tell her, quite naturally, “I’m trusting you with this.” It’s only for her little brother, but she is in control of how and when it is spent. She holds that $20 in trust for her brother.

That’s a simple trust. The trust is not just the $20—it’s also the special relationship between that $20, your daughter, and your son.

There’s a legal term for each person involved. You are the grantor, because the money was originally yours and you are the one entrusting it to someone else and giving them instructions. Your teenage daughter is the trustee, because she’s the one who possesses the money and must follow your instructions about how and when and for whom it is spent. Your young son is the beneficiary, because this whole arrangement is for his benefit.

A simple trust.

You have more power over your property than you think

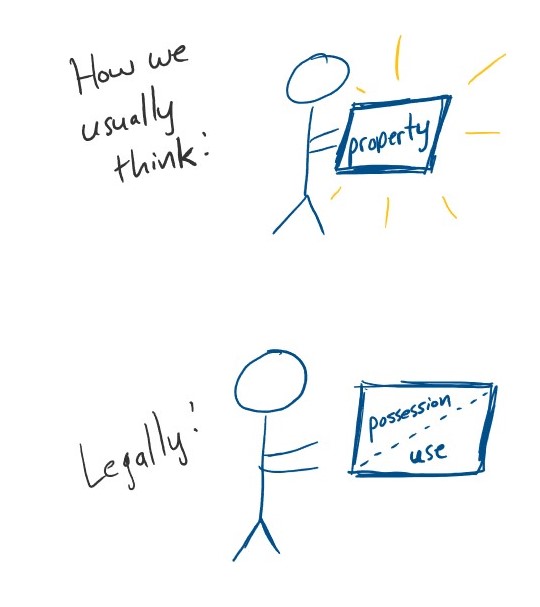

It helps to understand that when you create a trust, you are exercising your legal rights as owner of your property in a different way than normal.

Most of the time, we think that owning property means one thing: it’s mine and I can do what I want with it. You can go a little deeper, though, and think about all the things you can do with it. For example, let’s say you are the proud and fortunate owner of an apple. You own it, sure, but what does that mean? What can you do with that ownership? Well, you can:

Control where the apple is, physically (in your hands, for example, or in your cupboard)

Eat the apple

Feed the apple to your child

Plant the apple seeds

Throw the apple in the garbage

Give the apple to someone else

Think of each of these things as a different legal right you have as owner. The thing is, owning the apple is not an all-or-nothing game. You can divvy up these rights and uses and give them to different people. You can just hand the entire apple to someone else, sure. But you could also cut it in half and keep some for yourself. You could take the seeds out first and give them to a different person. You could hand the apple to your friend to keep safe for you while you go take a swim.

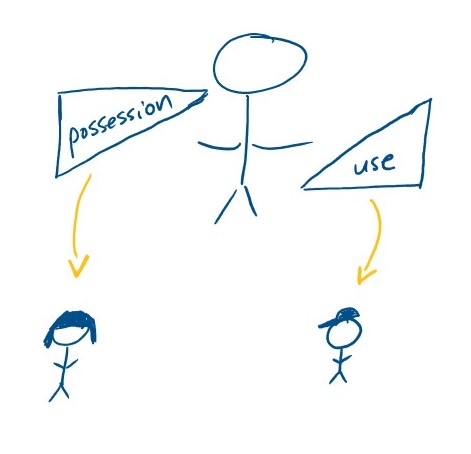

Think of ownership as a bunch of separate rights over the property. These rights, such as the right to possess and the right to use, can be separated by creating a trust.

In the same way, when you create a trust, you’re dividing the different rights to your property and giving them to different people. You’re giving the right to possess and manage the property to your trustee, and you’re giving the right to use and enjoy the property to your beneficiary.

Of course, it gets a little more complicated than that. When you give these different rights to different people, you also have to create some rules about what each person can and cannot do with the property. Does the trustee get paid for the job? Can your beneficiary use the trust money to buy a luxury car? You might want to answer these questions.

Trusts are about the future

In fact, the great benefit of a trust is it allows you to set the rules and control how your property is going to be used and managed far into the future. Most of us only think about our property in the here and now, making decisions about how to invest it or manage it or spend it as they come. In fact, we all have the creative power to set legally enforceable rules and relationships between our property and the people we love.

Why would you want to do that? I’ll answer that question in future articles. In short, though, you create a trust because you want to set your own rules for who is going to control your property and how it is going to be used in the future. You want to do that because it will protect or help your family. Because, as with our example of the county fair, sometimes handing over a wad of cash is not the best way to do it.

https://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.png00Benjaminhttps://www.bswright.com/wp-content/uploads/2020/07/Wright-Logo-1.pngBenjamin2019-10-21 21:47:342022-01-07 18:27:58What is a trust, exactly?

Sir Ernest Gowers wrote Plain Words, a guide for the British Civil Service on how to write to members of the public. That is, he was telling bureaucrats how to “explain the law to the millions.” He gave three elementary rules:

Be short.

Be simple.

Be human.

Later in the book, he added a fourth:

Be correct.

I’ve never seen better guidewords for anyone whose job is to help ordinary people with law and the government. That’s not just those who work for a government agency, but also attorneys.

Sadly, both government workers and attorneys are often bad at following Gowers’s advice. We take 50 words to say what could be said in 10. We use legal jargon when plain English would work better. We write and speak like robots or Vulcans. We make ourselves difficult to understand.

I think we should change that. Short, simple, human, correct—when I do a will, trust, or Medicaid application, that’s what I want my client’s experience to be. In elder law, things often do become long and complicated. But I think my role as an attorney is to take a complicated legal task and make it as simple for my client as I can.

Here’s an example. Most estate planning done by lawyers takes one or two months and several in-person meetings to complete. These meetings can pack a lot into just one or two hours. A client might be asked to make many decisions in quick succession. It’s easy to succumb to decision fatigue.

Can’t we find a better way? A way to have fewer and maybe shorter meetings? A way to educate clients and give them time to make good decisions? A way to make the estate planning process less of a hassle?

I haven’t figured it out yet. But I want to. I have some ideas that are worth trying. Because whatever the status quo is, it’s not short, simple, or human. And it’s not working—most Americans have little or no estate planning in place.

Talking about simple, that’s one thing Medicaid is not. It’s a huge and complicated government program, which many people depend on for long-term care. I can’t make Medicaid simple. I can’t change the rules or get my clients through some loophole that magically solves everything. But I can make it simpler. I can make it less complicated for my clients.

I wish the world operated on Gowers’s rules. I wish wills, trusts, and Medicaid applications were all short, simple, human, and correct—they are often none of those things. I think my job—and the job of everyone who works in estate planning or elder law—is to bring as much brevity, simplicity, humanity, and accuracy as I can to my work.